Summary

The Land-Credit Feedback Loop (also called the “property-credit nexus” or “financialisation of land”) describes the post-1970s structural mechanism by which bank credit and land prices mutually reinforce each other. Rising land prices enable more bank lending (against rising collateral); more bank lending drives more demand for land; higher demand raises prices further. This self-reinforcing cycle — absent during the Bretton Woods / post-war capital control era — emerged when financial deregulation allowed banks to switch from business lending to mortgage lending. Josh Ryan-Collins, Toby Lloyd, and Laurie Macfarlane (2017) provide the primary academic documentation in Rethinking the Economics of Land and Housing. Their argument is that this loop is the key mechanism explaining why house prices have outpaced incomes and GDP since the 1970s, and why financial crises are now longer and deeper than standard business cycles.

Mechanism

Stage 1: Deregulation Unlocks the Loop

- Pre-1970s: Banks primarily lent to businesses for productive investment; property lending was regulated and limited

- Post-1970s: Deregulation allows banks to shift dramatically toward mortgage/property lending

- Land becomes the dominant form of bank collateral in modern economies

- Regulatory incentives (Basel risk weights) further favor property lending over business lending [Source: Ryan-Collins et al., 2017, Ch.1, p.13]

Stage 2: The Self-Reinforcing Cycle

- Banks lend against rising land collateral

- Borrowers use credit to bid for land → prices rise

- Rising prices increase collateral value → banks lend more

- More lending → more demand → prices rise further

- Cycle continues until either: (a) borrowers can’t service debt at current rates, or (b) land prices stop rising (removing the expected return that justified prices)

- When prices stop rising → they fall (no equilibrium plateau — overpricing must correct)

Stage 3: The Bust

- Borrowers default → banks hold overvalued collateral

- Banks must choose: write down (take losses) or hold (freeze credit for years/decades)

- Japan 1990s: chose to hold → “lost decade” extended to two decades

- 2008: “creative” destruction of mortgage-backed securities accelerated the reckoning

Evidence: UK Land Prices vs. House Prices vs. Credit

- UK land prices (real, since WWII): +1,500% (15x)

- UK house prices (real, since WWII): +500% (5x)

- Land price volatility dwarfs house price volatility — three major boom-bust cycles (1970s, late 1980s, 2000s) correspond exactly to credit expansions [Source: Ryan-Collins et al., 2017, Ch.1, Figure 1.1]

- House price volatility is “primarily driven by land values” — construction costs move slowly; land prices are the swing factor

What Makes Land Different from Other Collateral

- Supply of land is fixed (cannot produce more) → rising demand must be met by rising prices

- Land cannot depreciate (unlike buildings, machines, inventory)

- Land does not respond to rising prices by increasing supply (unlike other commodities)

- This means: unlike standard collateral (inventory, equipment), land never triggers the corrective supply response that equilibrates other markets

- Result: a self-reinforcing loop with no natural brake except debt-service limits

UK Three Boom-Busts (Ryan-Collins, 2017)

Ryan-Collins documents three UK boom-bust cycles as direct consequences of mortgage credit liberalization:

- 1970s boom-bust: Post-1971 Competition and Credit Control deregulation allowed banks to expand mortgage lending; house prices surged then crashed with oil shock [Source: Ryan-Collins et al., 2017]

- 1980s boom-bust: Thatcher financial deregulation; building societies converted to banks; 95%+ LTV mortgages appeared; late 1980s bubble then early 1990s crash [Source: Ryan-Collins et al., 2017]

- 2000s boom-bust: Basel II risk weights favored property (50% weighting for residential vs. 100% for business lending); securitization via RMBS/MBS spread risk globally; crash of 2007–2009 [Source: Ryan-Collins et al., 2017]

In each case: credit liberalization → mortgage expansion → land price surge → feedback loop → crisis

Mortgage Securitization as Modern Amplifier

Ryan-Collins explicitly identifies mortgage securitization (MBS/RMBS) as the bubble amplifier that transformed a national credit cycle into a global financial crisis in 2007–2009:

- MBS divorced mortgage origination from credit risk holding (“originate to distribute” model)

- Removed natural check on lending quality: lenders no longer held the downside

- Allowed unprecedented leverage on land collateral across global capital markets

- Result: the 2008 crisis was far larger and more global than prior cycles [Source: Ryan-Collins et al., 2017]

Ryan-Collins Full Analysis — Financialisation (Ch. 5)

Ryan-Collins et al. (2017) document the four-stage activation of the modern loop:

- Financial deregulation (1970s–1980s): Capital controls lifted, reserve requirements abolished. By 2007, banks in most advanced economies had become primarily real estate lenders — a complete reversal of 1928 and 1970 lending profiles. [Source: Jorda et al., 2016, cited in Ryan-Collins 2017]

- Endogenous credit creation activates the loop: Rising land prices raise collateral values → banks create new purchasing power (mortgages) → demand for land rises → prices rise. Money flows into a fixed-supply asset, producing pure price inflation rather than productive investment.

- Expectations and leverage amplify: Expectations of capital gains draw additional buyers. Leverage amplifies gains on the way up and losses on the way down (forced selling when collateral < debt).

- Crisis and debt deflation: Land price peak → credit contraction → falling collateral → bank insolvency risk → recession. 2008 US/UK/Ireland/Spain all followed this exact sequence.

Key empirical data (UK):

- Mortgage debt to GDP: ~20% (1980) → ~80% (2007)

- Bank lending share going to real estate: ~35% (1986) → ~75% (2008)

- House price real growth: ~400% from 1980–2010 vs. ~100% income growth — gap entirely explained by rising land values [Source: Ryan-Collins et al., 2017]

International validation: Singapore, Denmark, Taiwan — countries with stronger Land Value Tax systems — show markedly lower credit-land amplification and smaller boom-bust cycles. [Source: Ryan-Collins et al., 2017]

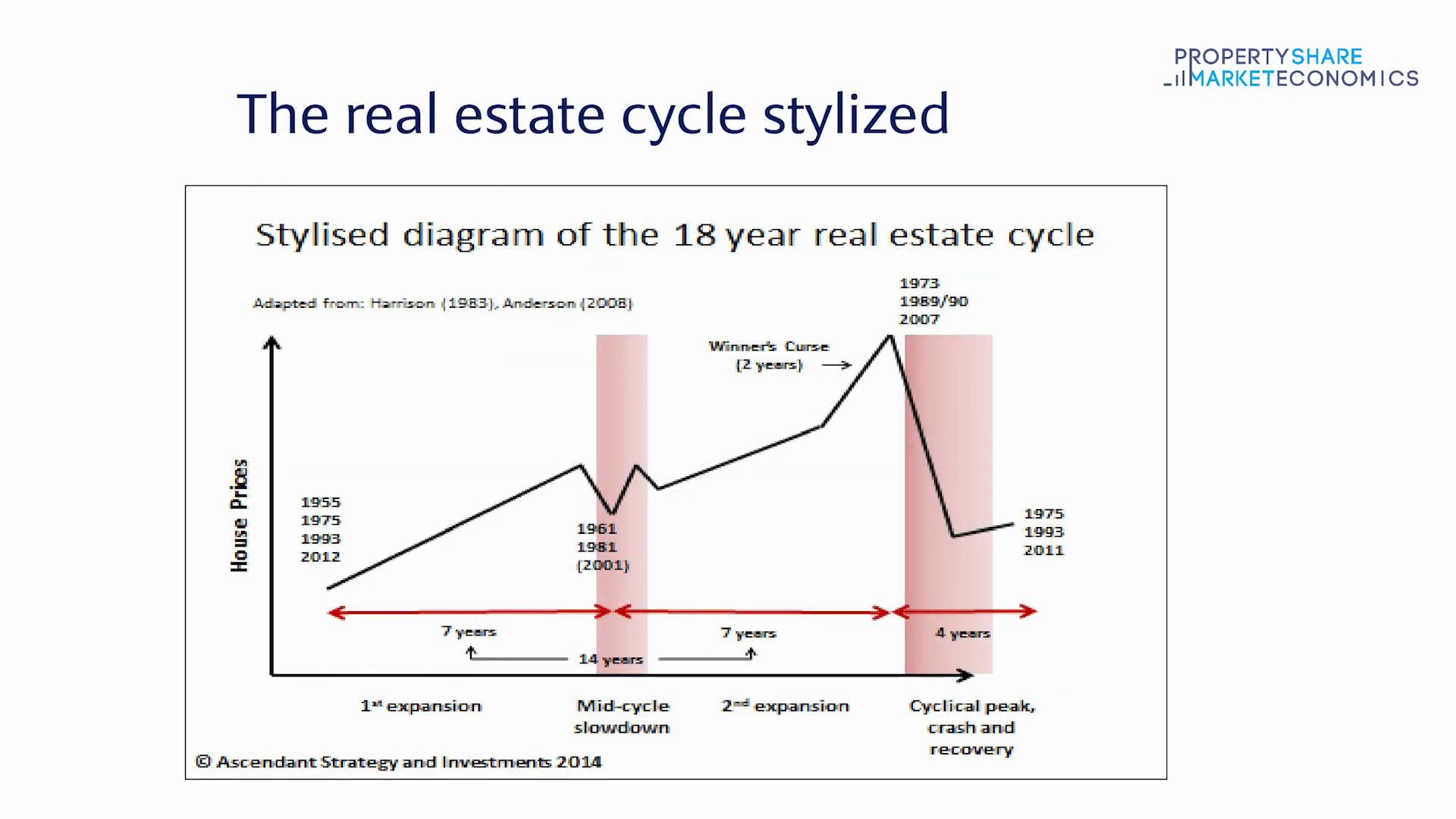

Connection to the 18.6-Year Cycle

The Land-Credit Feedback Loop is the modern credit mechanism that powers the broader 18.6-year real estate cycle:

- The Georgist/Hoyt cycle describes the land speculation pattern (18-year average)

- The Loop describes the amplifier — why post-1970 cycles have become more extreme

- Gaffney’s Element 6 (“Lending for overpriced land weakens banks”) describes the same mechanism [Source: gaffney-role-of-land-markets-2009.pdf]

- Foldvary’s Austrian component (credit expansion distorting rates) is the Loop’s monetary analog

Ryan-Collins’s methodological position is that the modern 18-year cycle is credit-driven: pre-credit-deregulation periods (1945–1970) showed suppressed cycles. Harrison, Anderson, and Foldvary treat the cycle as structural across centuries. Both can be true: the 18-year period may be an intrinsic land-speculation rhythm that was suppressed by capital controls and reactivated post-1970 by credit liberalisation.

Policy Implications

Ryan-Collins et al. propose multiple reforms to break the loop:

- Land Value Tax — imposes annual carrying costs on land, removing speculative buy-and-hold incentive

- Banking regulation — limit banks’ ability to use land as collateral; require higher capital against mortgage lending

- Planning reform — reduce speculation by making development more predictable

- National accounting reform — separately track land values from building values to make the loop visible

- Ownership reform — expand community land trusts, public ownership

PSE Relevance

Phil Anderson’s framework implicitly relies on this loop — his observation that the “winners curse phase” sees land being financed by ever-more-leveraged credit directly maps to this mechanism. The PSE Clock’s “afternoon” phases (3pm–6pm in the current cycle reading) correspond to the loop running at maximum intensity before collapse.

Notable Quotes

“The last few decades have seen an extraordinary growth in real-estate related credit, in particularly for mortgage lending: what we call the ‘financialisation’ of land. The chapter argues that the move towards home ownership as the preferred form of tenure and the liberalization of the banking sector have led to the emergence of a feedback cycle between land and credit that has come to dominate modern economies.” — Ryan-Collins et al. [Ch.1, p.15]

“Capitalist economies are characterized by a land-credit ‘cycle’, which may be longer and deeper than the standard economics’ textbook ‘business-cycle’.” — Ryan-Collins et al., citing Borio (2014)

“Rapid rises in real-estate credit lead to increased financial fragility and are strong predictors of financial crises and long-lasting recessions.” — Ryan-Collins et al. [Ch.1, p.13]

Contradictions & Open Questions

- Ryan-Collins argues the cycle is credit-driven (suppressed in the Bretton Woods era); Harrison/Anderson/Foldvary treat it as structural across centuries. Both positions may be compatible but the tension is not resolved.

- If the loop is fundamentally about credit liberalization, does the cycle weaken if macroprudential regulation curtails mortgage lending? The historical evidence (Singapore, Taiwan) suggests yes, but post-2010 macro-pru experiments are still too recent to confirm.

- The “originate to distribute” securitization model that amplified the 2008 crisis still largely exists — has its risk been contained by post-GFC regulation, or merely suppressed until the next cycle?

Bird’s Corroboration — The “Land Standard” and Productivity Drain

Mike Bird (The Land Trap, 2025) provides a mainstream-economics corroboration of the feedback loop with two notable extensions:

1. The Land Standard: Bird documents Japan’s pre-1990 economy as running on tochi hon’isei (“Land Standard”) — the economy was effectively pegged to land values the way currencies were once pegged to gold. Companies used land as collateral to access credit; rising land values enabled more borrowing; borrowed money went back into land. When land fell >80% in urban cores, the loop ran in reverse: collateral collapsed, banks accumulated non-performing loans that eventually reached 123 trillion yen (~25% of GDP) by 1998. “Between 1989 and 2004, the cumulative capital loss of land alone ran to one quadrillion yen, around $8 trillion USD at today’s exchange rate.” [Source: Bird, The Land Trap, 2025, Ch. 7]

2. The Productivity Crowding-Out Channel: Bird’s most distinctive empirical contribution is documenting that land booms misallocate credit during the boom, not just at the crash:

- Banque de France research: a 10% rise in real estate prices boosts investment by land-rich firms but lowers investment by land-poor firms

- BIS economist Sebastian Doerr: land-rich firms are less productive than their land-poor peers; the surge in real estate prices 1993–2008 was large enough to drag down productivity of entire sectors

- Firms borrowing from banks in the hottest housing markets paid higher interest rates, borrowed less, and invested far less than peers elsewhere (Chakraborty, Goldstein, MacKinlay, 1988–2006)

- Post-2008, banks became more mortgage-heavy as they repaired balance sheets, binding land and finance even more tightly [Source: Bird, The Land Trap, 2025, Ch. 6]

This adds a new dimension to the loop: the credit misallocation is not just a financial problem but a real-economy productivity problem that builds during the entire upswing.

Key Sources

- 2026-05-03-ryan-collins-rethinking-land-housing-ch1 — primary book source

- 2026-05-03-ryan-collins-bsp-lecture-transcript — lecture with UK data charts

- 2026-05-03-gaffney-role-of-land-markets-2009 — Gaffney’s parallel diagnosis

- 2026-05-04-ryan-collins-rethinking-economics-land-housing — Ch. 5 full analysis

- 2026-05-15-the-land-trap-mike-bird — Bird (2025): Japan Land Standard, 2008, China; productivity crowding-out channel

Cross-References

- 18.6-Year Real Estate Cycle — the broader cycle this mechanism operates within

- Geo-Austrian Synthesis — Foldvary’s theory describing the same credit amplification from a different angle

- Economic Rent — the rent captured by land owners that drives speculative demand

- Property Tax as Cycle Stabilizer — the primary policy prescription to break this loop

- Land Value Theory — foundational theory

- Bubble Amplifiers — securitization as the modern mechanism